Options are flexible instruments, but that flexibility is exactly why I do not like treating them as shortcuts. A call option, a put option, and a few strike prices can be combined into many different payoff shapes. Some strategies are built for income. Some are built for hedging. Some are built for directional trades. Others […]

10 Options Strategies Every Investor Should Know

Options are flexible instruments, but that flexibility is exactly why I do not like treating them as shortcuts. A call option, a put option, and a few strike prices can be combined into many different payoff shapes. Some strategies are built for income. Some are built for hedging. Some are built for directional trades. Others are built around volatility, time decay, or a defined price range.

When I look at an options strategy, I first ask five questions: What is my market view? What is my volatility view? How much premium am I paying or receiving? Where are my breakeven points? What happens if I am wrong before expiry?

That framework matters more than memorising names. A covered call, a bull call spread, and an iron condor may all use options, but they solve very different problems. In Indian markets, where traders often track Nifty, Bank Nifty, weekly expiries, option chains, open interest, and Greeks, the same strategy can behave very differently depending on expiry, liquidity, implied volatility, and execution.

This guide explains 10 options strategies every investor or active options trader should know. It is educational, not investment advice. Options trading involves market risk, and every strategy should be tested, sized, and understood before real capital is used.

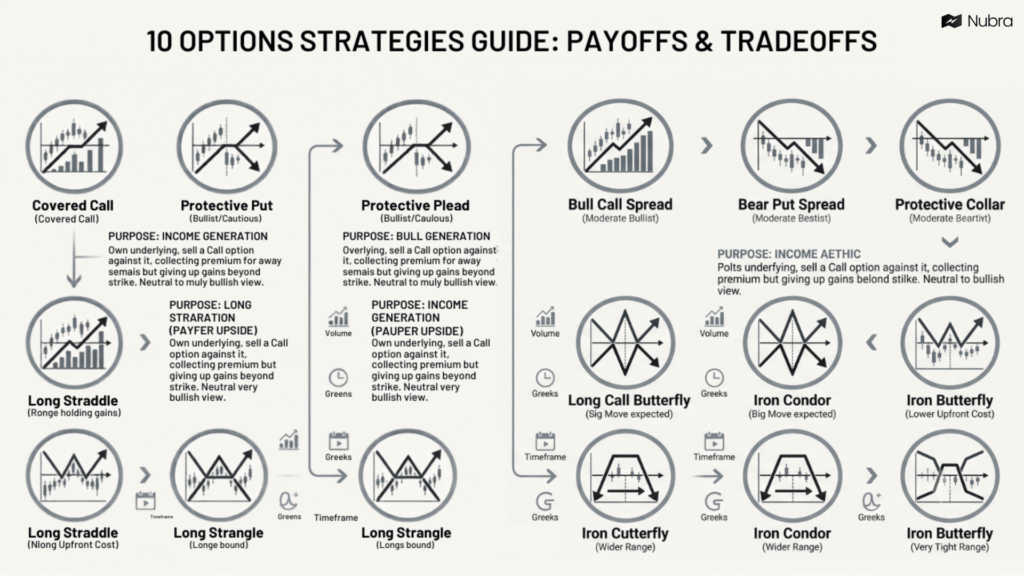

Quick Comparison of the 10 Options Strategies

| Strategy | Market view | Typical structure | Risk profile |

|---|---|---|---|

| Covered call | Neutral to mildly bullish | Own underlying and sell a call | Downside remains in the holding; upside is capped |

| Protective put | Bullish but cautious | Own underlying and buy a put | Put premium is the cost of protection |

| Bull call spread | Moderately bullish | Buy lower strike call, sell higher strike call | Limited loss and limited profit |

| Bear put spread | Moderately bearish | Buy higher strike put, sell lower strike put | Limited loss and limited profit |

| Protective collar | Holding gains, wants a hedge | Own underlying, buy put, sell call | Downside cushioned, upside capped |

| Long straddle | Big move expected, direction unclear | Buy call and put at same strike | Loss limited to premium; needs large move |

| Long strangle | Big move expected, lower upfront cost than straddle | Buy OTM call and OTM put | Loss limited to premium; needs even larger move |

| Long call butterfly | Range-bound, precise target | Buy one lower call, sell two middle calls, buy one higher call | Limited risk and reward |

| Iron condor | Range-bound, low-volatility view | Sell OTM put spread and OTM call spread | Defined risk, defined reward |

| Iron butterfly | Very tight range view | Sell ATM call and put, buy wings | Defined risk, defined reward |

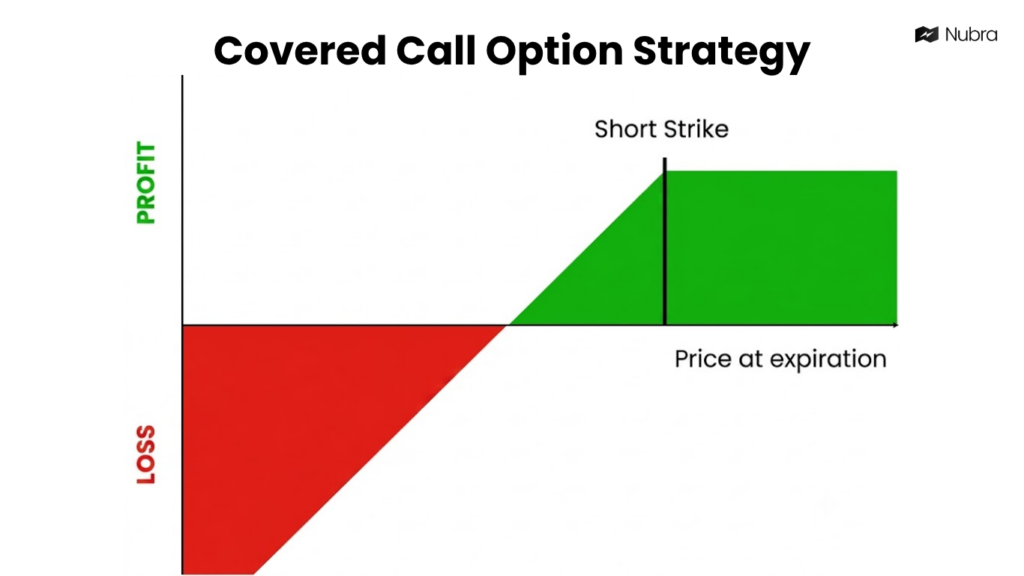

1. Covered Call

A covered call combines a long holding with a short call option. In simple terms, the trader already owns the stock or underlying exposure and sells a call option against it. The premium received creates income, but the upside is capped beyond the call strike.

For example, if I hold a stock at Rs 1,000 and sell a Rs 1,080 call, I collect a premium. If the stock stays below Rs 1,080 by expiry, the call may expire worthless and I keep the premium. If the stock moves sharply above Rs 1,080, I may have to give up gains beyond that level because the short call offsets my upside.

I would think about a covered call only when my view is neutral to mildly bullish, not aggressively bullish. The mistake is selling calls on a holding I still expect to rally strongly. In that case, the premium can feel small compared with the upside I give away.

In a trading workflow, I would check the option chain for liquidity, implied volatility, and the premium available at different strikes. Higher premiums are not automatically better. They may simply reflect higher expected movement. Position size and lot size also need to make sense for the capital at risk.

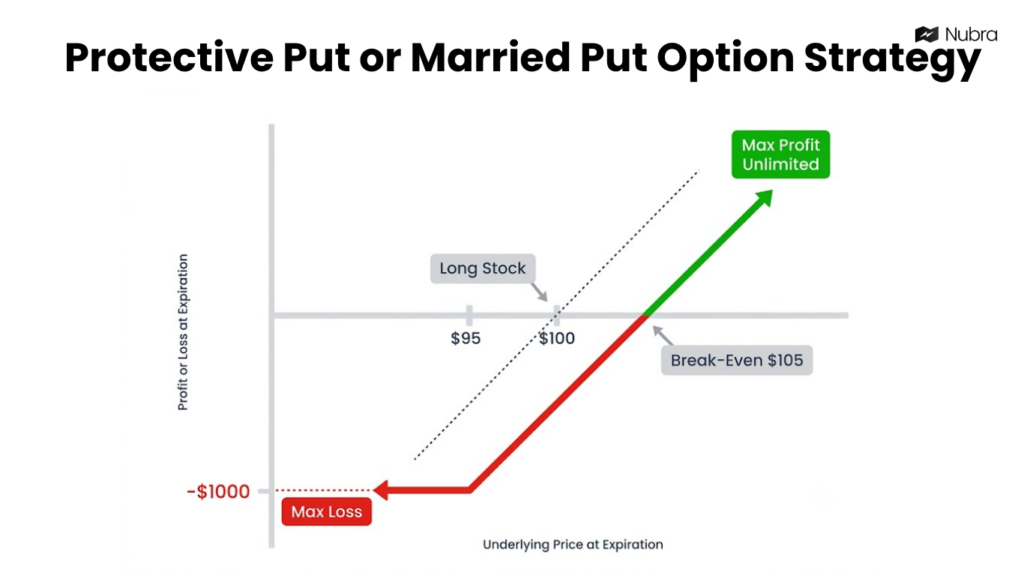

2. Protective Put or Married Put

A protective put is a hedge on an existing long position. The trader owns the underlying and buys a put option so that, if the price falls sharply, the put can gain value and offset part of the loss.

Think of it like paying a premium for downside protection. If I hold a stock or index exposure and buy a put below the current price, I am defining a level where I want protection to begin. If the market rises, the put may expire worthless, and the premium paid becomes the cost of staying protected.

The main trade-off is cost. A protective put can be useful around event risk, market uncertainty, or when I want to stay invested but do not want unlimited downside exposure over a specific period. But if I keep buying protection too often, the premium cost can eat into returns.

For Indian F&O traders, this is where expiry selection matters. A near-expiry put may be cheaper but decays faster. A further-expiry put may offer more time but costs more. I would compare the hedge cost against the actual risk being reduced, rather than buying a put just because the market feels uncertain.

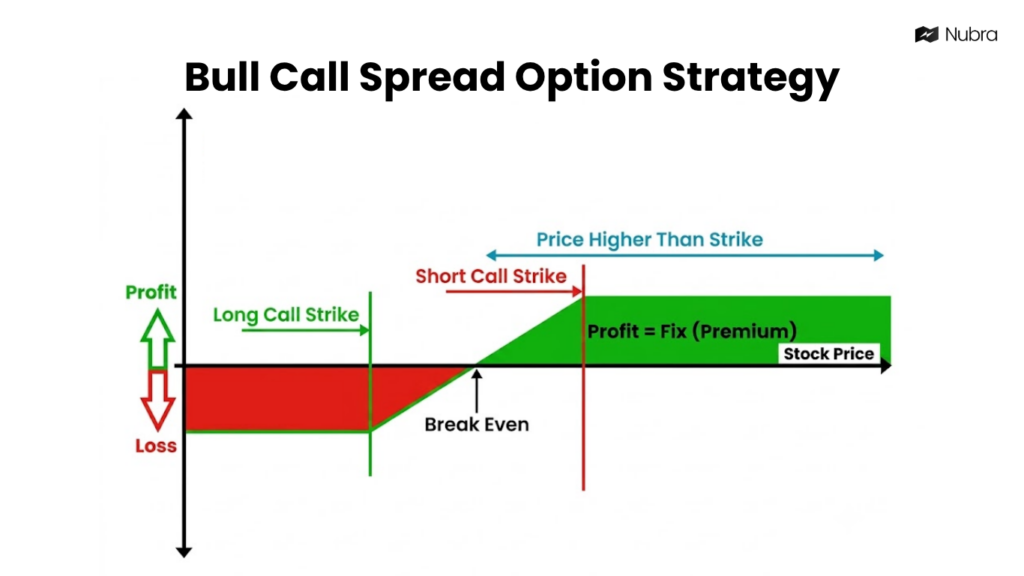

3. Bull Call Spread

A bull call spread is a defined-risk bullish strategy. It buys a call option at a lower strike and sells another call at a higher strike, usually with the same expiry. The sold call helps reduce the upfront premium, but it also caps the maximum profit.

For example, if Nifty is near 25,000 and I expect a moderate move higher, I might buy a 25,000 call and sell a 25,300 call. The structure can work if Nifty rises, but the upside is limited beyond the higher strike. If Nifty does not move enough, the spread can lose money.

I prefer thinking of this as a “moderate bullish” setup, not a “maximum bullish” setup. If the view is for a very large upside move, a spread may feel restrictive because the short call caps the gain. If the expectation is only a measured move, the reduced premium can make the structure more practical than buying a naked call.

Before placing this kind of strategy, I would check the payoff chart, breakeven, maximum loss, and maximum profit. The name of the strategy matters less than whether the risk-reward makes sense after spreads, brokerage, taxes, and slippage.

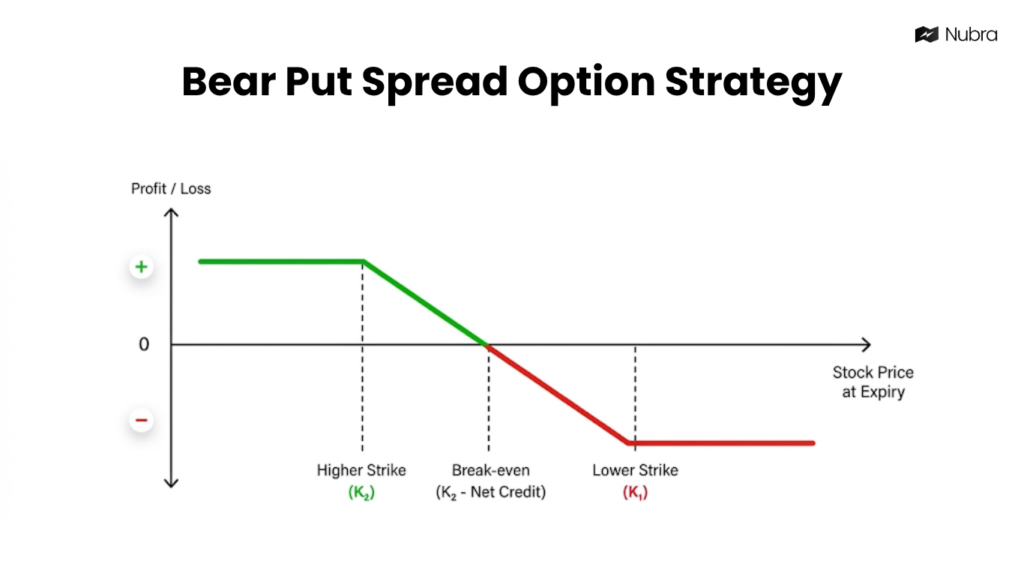

4. Bear Put Spread

A bear put spread is the bearish version of a defined-risk vertical spread. It buys a put at a higher strike and sells another put at a lower strike. The bought put benefits if the underlying falls, while the sold put reduces the cost but caps profit below the lower strike.

If Bank Nifty is trading near 55,000 and I expect a moderate decline, I might buy a 55,000 put and sell a 54,500 put. If Bank Nifty falls toward the lower strike, the spread can gain. If it falls far below the lower strike, the profit is still capped.

This structure can be more disciplined than buying a plain put when implied volatility is high. The sold put offsets part of the premium. But it also means the target zone should be clear. If the view is that the market can crash far beyond the lower strike, the spread may not capture the full move.

I would also be careful near expiry. Spreads can look simple on a payoff chart, but execution, liquidity, and rapid price changes matter. Wide bid-ask spreads can reduce the real-world advantage of a theoretically attractive setup.

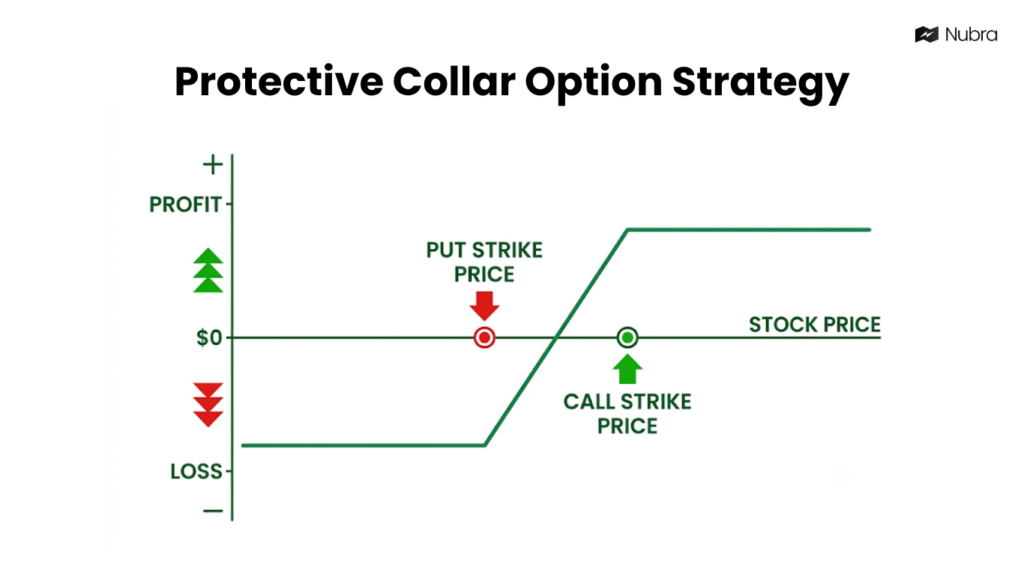

5. Protective Collar

A protective collar combines an existing long position, a long put, and a short call. The put cushions downside and the short call helps fund the cost of the put. In return, the position accepts a cap on upside.

This can be useful when I already have gains in a holding and want to protect them for a period without fully exiting. For example, if I hold a stock that has rallied, I may buy a put below the current price and sell a call above the current price. The put creates a floor, while the call creates a ceiling.

The collar is not a magic hedge. It changes the shape of the position. I reduce some downside, but I also give away some upside. That can be a reasonable trade-off if my priority is protecting a gain or managing event risk, but it is frustrating if the stock continues to rally sharply.

When evaluating a collar, I would look at the distance between the current price, put strike, and call strike. A tight collar offers more control but less room. A wider collar gives the position more breathing space but may cost more or protect less.

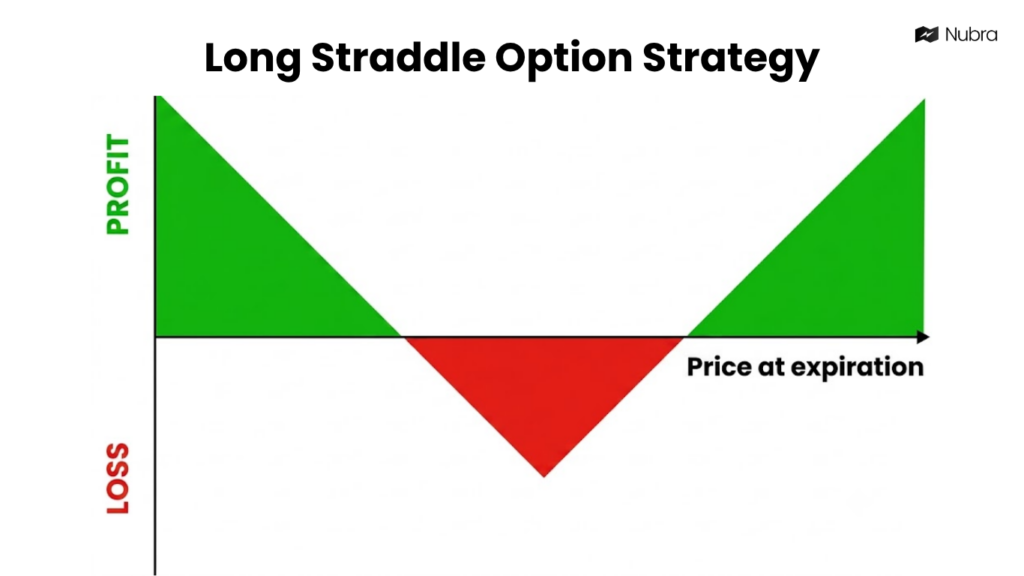

6. Long Straddle

A long straddle is a volatility strategy. It buys a call and a put at the same strike and expiry. The trade is not choosing direction; it is choosing movement. The strategy needs the underlying to move enough in either direction to cover the combined premium.

This is why I do not describe a straddle as a simple “profit from volatility” trade without qualification. If the market does not move enough, both options can lose value as time passes. The maximum loss is the premium paid, but that loss can still be significant if the options were expensive.

In India, traders often think about straddles around results, policy events, budget day, or expiry sessions. The key question is whether the expected move is already priced into implied volatility. If everyone expects a big move, the call and put may both be expensive. The market then needs to move even more than expected for the trade to work.

Before using a long straddle, I would check the combined premium and calculate both breakevens. If a 25,000 straddle costs 300 points, the upper breakeven is 25,300 and the lower breakeven is 24,700 before costs. That gives a clearer sense of how much movement the position actually needs.

7. Long Strangle

A long strangle is similar to a long straddle, but the call and put are bought at different out-of-the-money strikes. It usually costs less than a straddle because both options are OTM. The trade-off is that the underlying must move further before the strategy becomes profitable.

For example, if Nifty is at 25,000, I might buy a 25,300 call and a 24,700 put. This creates exposure to a large move in either direction, but the market has to travel farther than it would in an at-the-money straddle.

I would consider a long strangle when I expect a large move but want to reduce premium outlay compared with a straddle. I would avoid it when the market is likely to move only slightly, because both OTM options can decay quickly if the expected breakout does not arrive.

The natural mistake is choosing strikes only because they are cheap. Cheap options are often cheap for a reason: they may have a lower probability of finishing in the money. I would use the option chain, implied volatility, and payoff simulator to understand what move is required, instead of treating low premium as low risk.

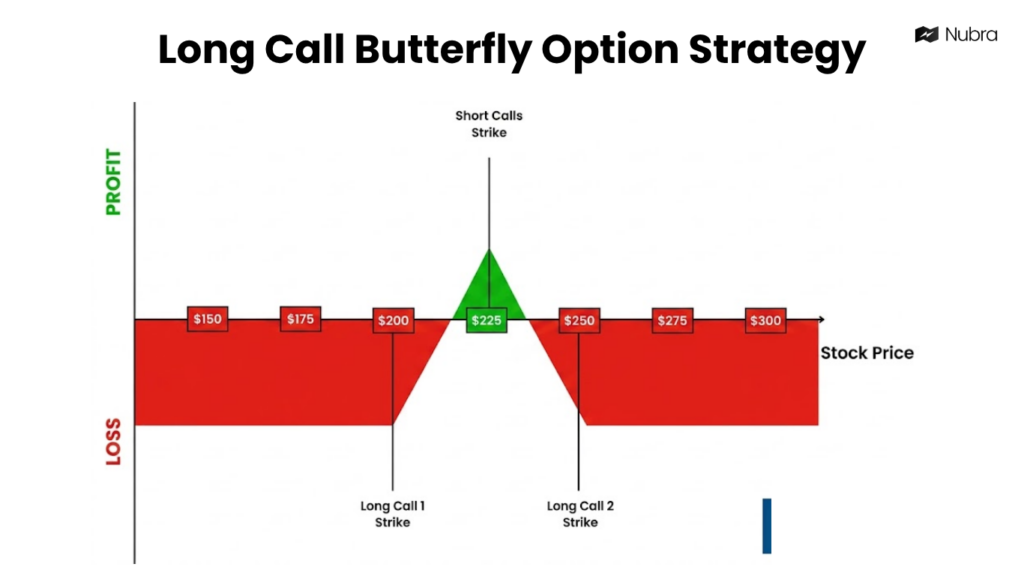

8. Long Call Butterfly

A long call butterfly is a range-bound strategy with three strike prices. A common structure is: buy one lower-strike call, sell two middle-strike calls, and buy one higher-strike call. The maximum profit is usually around the middle strike at expiry.

This strategy is more precise than many traders expect. It is not just a “sideways market” setup; it works best when I have a specific target zone and the underlying stays near that zone by expiry. If the price moves too far below or above the wings, the strategy can lose money, though the risk is defined.

For example, if I expect an index to settle near 25,000 by expiry, I might structure a butterfly around that middle strike. The lower and higher strikes define the wings. The payoff chart will show a tent-like shape, with the best outcome near the centre.

I would not use a butterfly casually in illiquid contracts. Execution quality matters because the strategy has multiple legs. If one leg is filled badly, the payoff may no longer match the clean diagram. This is where a strategy builder and payoff preview can help before placing orders.

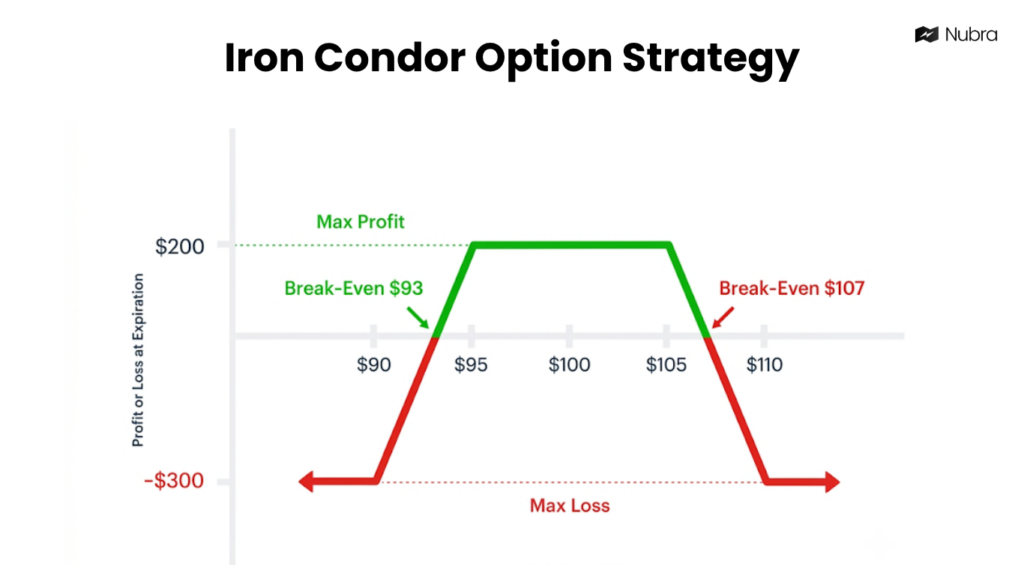

9. Iron Condor

An iron condor is a defined-risk range strategy. It combines a bull put spread below the market and a bear call spread above the market. The trader receives a net premium and wants the underlying to stay between the short put and short call strikes until expiry.

If Nifty is trading at 25,000 and I expect it to remain range-bound, an iron condor might involve selling a lower put spread and an upper call spread. The long options on both sides act as protection, so the maximum loss is defined. The maximum profit is generally the net premium received.

The iron condor is attractive because the risk is defined and the logic is easy to understand: stay inside the range. But the risk is not gone. A sharp trending move, volatility expansion, or poor adjustment can turn the position against me quickly.

When evaluating an iron condor, I would check three things: the width of the wings, the premium collected, and the probability of the underlying touching the short strikes. I would also be realistic about costs. Four-leg strategies can be sensitive to brokerage, taxes, bid-ask spreads, and exit timing.

10. Iron Butterfly

An iron butterfly is another defined-risk range strategy, but it is more concentrated than an iron condor. A typical structure sells an at-the-money call and put, then buys an out-of-the-money call and put as wings. The strategy receives a net credit and works best if the underlying stays close to the short strike.

Compared with an iron condor, an iron butterfly usually has a narrower profit zone. It can collect more premium because the short options are closer to the money, but it also needs the underlying to remain near the centre. That makes it more sensitive to movement.

For example, if Bank Nifty is near 55,000 and I expect a very tight expiry range, an iron butterfly could be built around the 55,000 strike with protective wings above and below. The payoff is defined, but the trade requires discipline because small moves can matter.

I would use this only when I understand how time decay, implied volatility, and gamma risk interact near expiry. A position that looks calm at entry can become difficult to manage if the underlying starts moving quickly near the short strike.

How I Would Choose Between These Options Strategies

I would not start with the strategy name. I would start with the market condition.

If I already own the underlying and want income, I would study a covered call. If I already own the underlying and want downside protection, I would study a protective put or collar. If the view is moderately bullish, I would compare a bull call spread against a plain call. If the view is moderately bearish, I would compare a bear put spread against a plain put.

If I expect a large move but do not know the direction, I would compare a straddle and strangle. If I expect a range-bound market, I would compare a butterfly, iron condor, or iron butterfly depending on how wide or narrow I expect the range to be.

The practical workflow is usually the same:

- Define the market view.

- Check the option chain for liquidity and open interest.

- Review implied volatility and Greeks.

- Build the payoff chart.

- Check maximum profit, maximum loss, and breakevens.

- Consider expiry, transaction costs, and exit plan.

- Paper trade or simulate before using real capital.

Nubra’s role in this kind of workflow should be decision support, not prediction. Where available, decision-support tools such as strategy builders, option-chain views, OI data, Greeks, payoff charts, and paper trading environments can help traders understand a setup before they trade. They do not guarantee that the market will behave as expected.

Conclusion

Options strategies are not just labels. They are ways to express a view on direction, volatility, time, and risk. The same trader may use a covered call for income, a protective put for hedging, a bull call spread for a moderate upside view, and an iron condor for a range-bound market.

The important part is to understand the payoff before the trade is placed. I would rather use a simple strategy with clear risk than a complex strategy I cannot manage under pressure. For Indian F&O traders, that means paying attention to expiry, liquidity, OI, Greeks, volatility, and execution quality.

This page is for educational purposes only and should not be treated as investment advice. Trading involves market risk, and strategy examples do not guarantee returns.

FAQs

What is the safest options strategy?

No options strategy is completely safe. Defined-risk strategies such as bull call spreads, bear put spreads, protective puts, collars, butterflies, iron condors, and iron butterflies can make the maximum loss easier to estimate, but they can still lose money.

Which options strategy is best for beginners?

Beginners usually benefit from first understanding calls, puts, payoff charts, premiums, expiry, and risk. Strategies such as covered calls and protective puts are easier to understand because they connect to an existing holding, but suitability depends on capital, risk tolerance, product permissions, and market knowledge.

What is the difference between a straddle and a strangle?

A straddle buys a call and put at the same strike and expiry. A strangle buys an out-of-the-money call and an out-of-the-money put with the same expiry. A strangle is usually cheaper, but it needs a larger price move to become profitable.

What is the difference between an iron condor and an iron butterfly?

An iron condor uses short strikes away from the current price and typically has a wider profit range. An iron butterfly sells the call and put near the same central strike, so it usually has a narrower profit zone and higher sensitivity to movement around that strike.

Why should I use a payoff chart before trading options?

A payoff chart helps me see the maximum profit, maximum loss, breakeven points, and expected behavior at expiry. It also makes the trade-off visible before I place a multi-leg strategy.

Disclaimer: The information provided in this blog is for educational and informational purposes only and should not be construed as investment advice, financial advice, or a recommendation to buy, sell, or hold any securities or financial products. Investments in the securities market are subject to market risks. Please read all related documents carefully before investing. Readers should conduct their own research and consult a SEBI-registered investment adviser or other qualified financial professional before making any investment decisions. Past performance is not indicative of future results.

Published Jul 14, 2026