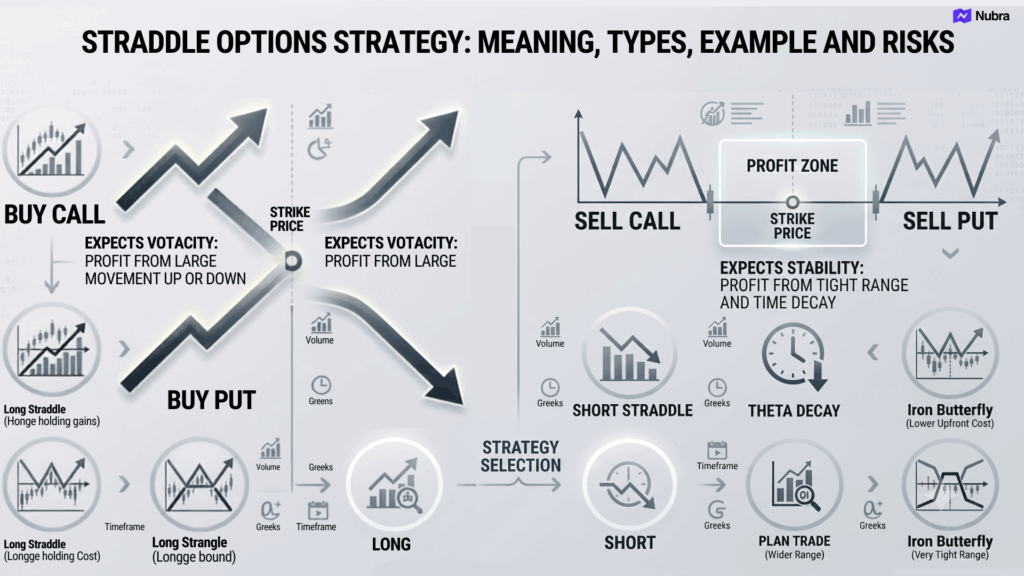

A straddle options strategy is a two-leg options strategy where I use a call option and a put option with the same underlying, same strike price, and same expiry. The idea is simple: instead of taking only a bullish or bearish view, I am taking a view on how much the market may move. In […]

Straddle Options Strategy: Meaning, Types, Example and Risks

A straddle options strategy is a two-leg options strategy where I use a call option and a put option with the same underlying, same strike price, and same expiry. The idea is simple: instead of taking only a bullish or bearish view, I am taking a view on how much the market may move.

In practice, a straddle can be created in two ways. In a long straddle, I buy both the call and the put. In a short straddle, I sell both the call and the put. Both use the same strike and expiry, but the risk profile is completely different.

This guide is for educational purposes only and should not be treated as investment advice. Options trading involves market risk, and outcomes depend on volatility, expiry, liquidity, execution, and individual decisions.

What Is a Straddle Options Strategy?

A straddle options strategy combines one call option and one put option at the same strike price and expiry. Traders usually study this strategy when they expect volatility but are not sure about direction, or when they expect the market to remain in a tight range.

For example, if Nifty is trading near 22,000, I may look at the 22,000 call option and the 22,000 put option for the same expiry. If I buy both, it becomes a long straddle. If I sell both, it becomes a short straddle.

The important part is that a straddle is not only about price direction. It is also about premium, time decay, implied volatility, and how far the underlying can move before expiry.

How a Straddle Strategy Works

In a long straddle, I pay a combined premium to buy the call and the put. The call can gain if the underlying moves up sharply, while the put can gain if the underlying moves down sharply. The losing leg may expire worthless, but the profitable leg can offset that loss if the move is large enough.

In a short straddle, I receive a combined premium by selling the call and the put. I benefit if the underlying stays close to the strike price and both options lose value. The risk is that a sharp move on either side can create losses larger than the premium received.

This is why I do not look at a straddle only as “buy both sides” or “sell both sides.” I first calculate the total premium, break-even levels, expected move, time left to expiry, and the risk if the market moves faster than expected.

Long Straddle vs Short Straddle

| Factor | Long Straddle | Short Straddle |

|---|---|---|

| Position | Buy call and buy put | Sell call and sell put |

| Market view | Large move expected, direction uncertain | Range-bound or low-movement view |

| Premium flow | Premium is paid | Premium is received |

| Maximum loss | Limited to total premium paid | Theoretically unlimited |

| Maximum profit | High on upside, meaningful on downside if move is large | Limited to premium received |

| Break-even | Strike plus/minus total premium paid | Strike plus/minus total premium received |

| Main risk | Market does not move enough before expiry | Market moves sharply in either direction |

| Volatility impact | Helps if implied volatility rises after entry | Helps if implied volatility falls after entry |

The same strike and expiry can therefore create opposite outcomes depending on whether I am buying or selling the straddle. A long straddle needs movement. A short straddle needs control, discipline, and a clear risk plan because a sudden move can expand losses quickly.

Straddle Options Strategy Example

Let me use a simple Nifty-style example.

Assume Nifty is trading near 22,000 and I am looking at the 22,000 strike for the same weekly expiry.

| Option leg | Action | Premium |

|---|---|---|

| 22,000 Call | Buy | Rs. 180 |

| 22,000 Put | Buy | Rs. 160 |

| Total premium paid | Rs. 340 |

If I create a long straddle, my total cost is Rs. 340. My break-even levels are:

| Break-even | Formula | Level |

|---|---|---|

| Upper break-even | 22,000 + 340 | 22,340 |

| Lower break-even | 22,000 – 340 | 21,660 |

This means the position needs Nifty to move above 22,340 or below 21,660 by expiry before the strategy becomes profitable, excluding costs such as brokerage, taxes, slippage, and execution differences.

If Nifty expires at 22,000, both options have no intrinsic value and the full premium is lost. If Nifty moves to 22,600, the call has intrinsic value of Rs. 600, while the put may expire worthless. After adjusting the Rs. 340 premium paid, the gross payoff is Rs. 260 per unit before costs. If Nifty moves to 21,400, the put has intrinsic value of Rs. 600, and the same gross payoff logic applies.

For a short straddle, the trade is reversed. I sell the 22,000 call and 22,000 put and receive Rs. 340. The maximum gain is the premium received if Nifty expires at 22,000. But if Nifty moves far above 22,340 or below 21,660, losses can begin to build beyond the premium collected.

When Traders Study a Long Straddle

I would usually study a long straddle when I expect a large move but do not want to choose the direction upfront. This can happen around results, policy events, major index reactions, or periods where the market has compressed and may break out.

The difficult part is that the move must be large enough and timely enough. If the options are already expensive because implied volatility is high, the market may move and the straddle may still disappoint after volatility cools. This is often called volatility crush, and it is one of the reasons a long straddle should be assessed before entry, not after the event has already inflated premiums.

When Traders Study a Short Straddle

I would study a short straddle only when I expect the underlying to remain within a range and when I have a defined risk-management plan. The appeal is clear: if the market stays near the strike, both options decay and the premium can reduce in value.

But the risk is also clear. A short straddle can look calm until a sharp move, gap, or volatility spike changes the payoff quickly. For that reason, traders often monitor the position closely, define exits, and avoid treating premium received as guaranteed income.

How to Read the Strategy Before Using It

Before I evaluate a straddle, I prefer to look at five things.

First, I check the total premium. The premium tells me how much movement the position needs. Second, I calculate both break-even points. Third, I compare those levels with the recent trading range, event calendar, and option-chain data. Fourth, I check time to expiry because theta can hurt long straddles and help short straddles. Fifth, I ask what happens if the market opens with a gap or if implied volatility changes sharply.

This is where an options workflow can help. An option chain, payoff chart, strategy builder, or paper-trading view can make the risk clearer before considering a live trade. The tool does not make the strategy profitable by itself, but it can help me compare scenarios, understand payoff changes, and avoid entering a position without knowing the break-even range.

Benefits and Risks of a Straddle Strategy

A straddle can be useful because it separates the market-movement view from a pure directional view. With a long straddle, I can study a setup where direction is uncertain but movement is expected. With a short straddle, I can study a range-bound setup where premium decay is the main idea.

The risk is that the market may not behave within the expected time frame. A long straddle can lose money if the move is late, slow, or already priced into expensive premiums. A short straddle can lose much more than the premium received if the market moves sharply. Execution also matters because bid-ask spreads, liquidity, slippage, brokerage, taxes, and sudden volatility changes can affect the final outcome.

FAQs

What is a straddle options strategy?

A straddle options strategy uses a call option and a put option with the same strike price, same expiry, and same underlying. It can be created by buying both options or selling both options.

What is the difference between a long straddle and a short straddle?

In a long straddle, I buy the call and put and need a large move to cover the premium paid. In a short straddle, I sell the call and put and benefit if the underlying stays close to the strike, but the risk can be high if the market moves sharply.

How do I calculate break-even in a long straddle?

For a long straddle, the upper break-even is the strike price plus total premium paid. The lower break-even is the strike price minus total premium paid.

Is a straddle strategy profitable in every market?

No. A straddle strategy is not profitable in every market. A long straddle needs enough movement before expiry, while a short straddle needs the market to stay within a range. Both can lose money.

Why is implied volatility important in a straddle?

Implied volatility affects option premiums. If volatility rises after a long straddle is entered, it can help the position. If volatility falls sharply, it can hurt the position. For a short straddle, falling volatility may help, while rising volatility may increase risk.

Should beginners use a straddle options strategy?

Beginners should first understand option premiums, Greeks, expiry, liquidity, and risk management before studying straddles. The strategy may look simple because it has two legs, but the payoff can change quickly with volatility and time decay.

Disclaimer: The information provided in this blog is for educational and informational purposes only and should not be construed as investment advice, financial advice, or a recommendation to buy, sell, or hold any securities or financial products. Investments in the securities market are subject to market risks. Please read all related documents carefully before investing. Readers should conduct their own research and consult a SEBI-registered investment adviser or other qualified financial professional before making any investment decisions. Past performance is not indicative of future results.

Published Jul 16, 2026